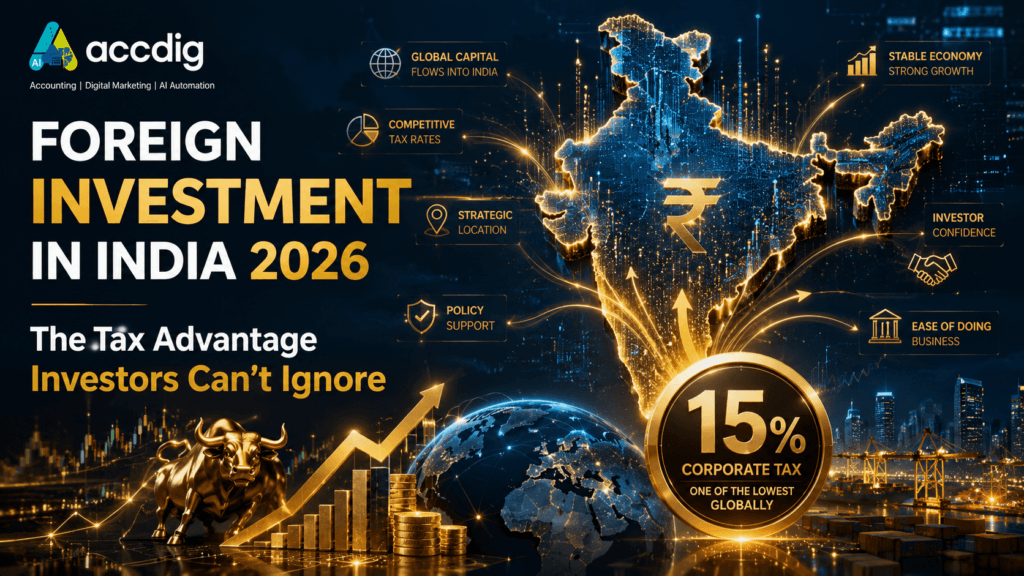

Hidden Edge: India Corporate Tax Rate & 2026 FDI

Let’s be blunt. For the past five years, whenever I have chatted with any founder, both of us have been looking at our products with the other one looking at her/his compliance dashboard. It’s not the issue of if we’re able to build it or not. Can we make it work to our global investors, while developing it here?

With the start of 2026 fast approaching, the world capital market is under stress. Growth is not all investors are after, they are looking for efficiency. And that is when that seemingly super dull number – the India corporate tax rate – just soars to the top of your pitch deck.

But it’s no talk of policy-wonks. This is in regards to your walk of the red carpet. It has to do with your valoration. This is in relation to who will sign the term sheet – Singapore or Silicon Valley VC looking closely at the impact of corporate tax on FDI.

Over the years, more complicated ‘cat and mouse structuring’ has evolved between the founders and foreign funds. It became a default when Singapore Flip (stand up of a Singapore holding company) became a failure. Why? For India it was thought that it was a high tax, high friction place.

The basis has been altered though. The changes to the policy which have been made in recent years are now “firmly in place” and the figures for foreign investment in India are getting too large to ignore. This article doesn’t present the Government’s Press release, it is an analysts look into the development of this new tax environment and what you as a founder or analyst must do with it to take advantage of it in investment in India 2026.

The Welcome Mat Analogy: Why Tax is Not Only a Number.

To my customers I always tell them: if you are thinking of doing business in a foreign country, then the first thing you should consider is the corporate tax rate of that country, which you can just treat as the welcome mat in front of the door to your business.

A low rate and clear and predictable corporate tax rate communicates the message ‘Welcome, we are here to do business and we will not stumble you. It signals partnership.

A high rate, a complicated rate or (worse yet) an unforeseen rate is a holey mat. Investors will be hesitant to invest, as they will not want to become involved in compliance issues, or risk losing their investments if they are sold for any reason.

Mat – a complex issue in India in the decades. It was overloaded with surcharges, cesses as well as with the much feared Dividend Distribution Tax (DDT). The DDT was not well-liked by the investors. It was like it was double taxed and had been a nightmare to return profits.

By taking the steps to lower the corporate tax rate for taxable income of the corporates and more importantly to drop DDT, it went against the fiscal stance of the government to provide a fiscal stimulus. We did not have to cross the mountain, we had to cross the mind. The message was loud and clear and to the world capital: “We are listening. We want to clear the way for foreign investment in India. The mat is clean.”

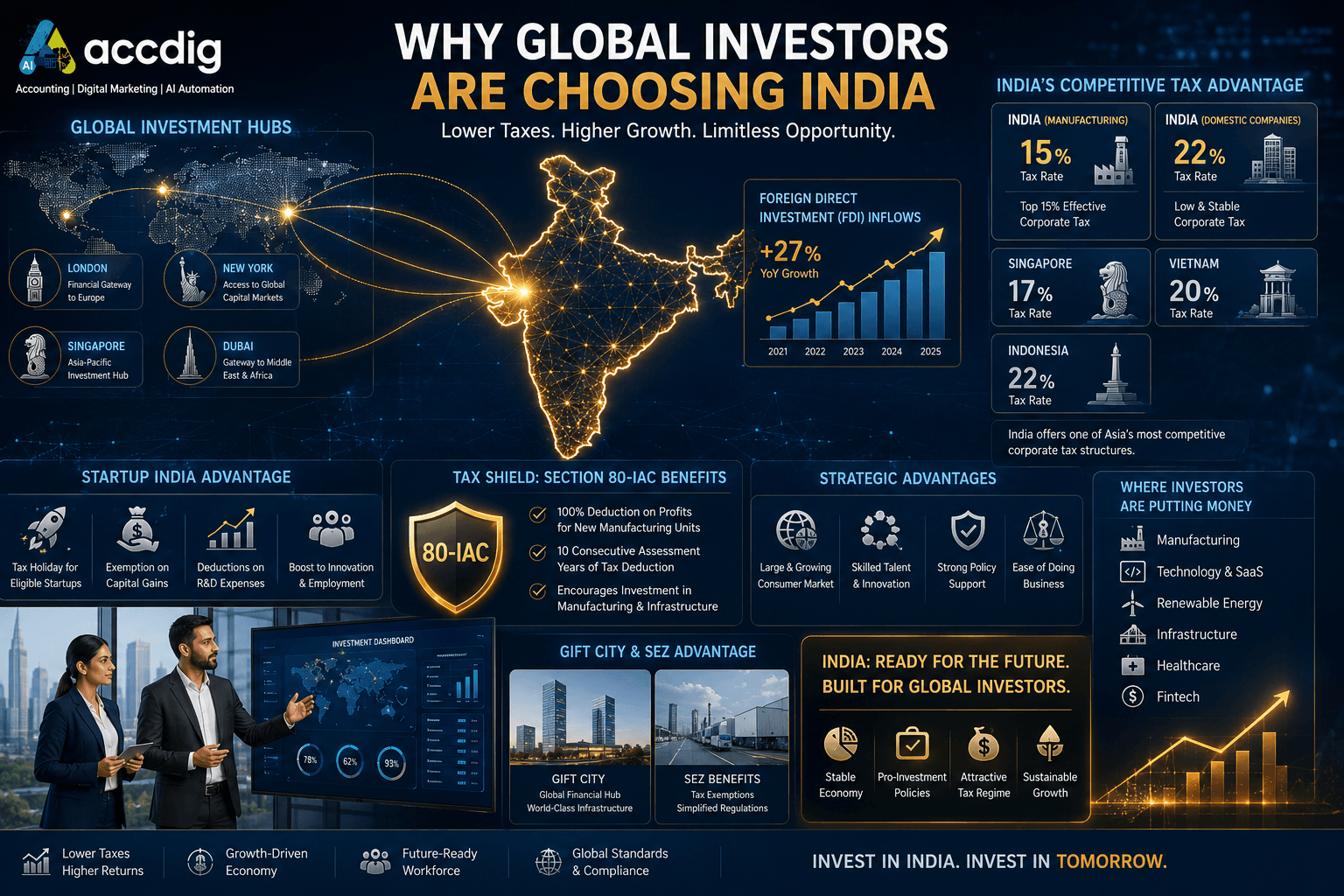

The Global Battlefield: vs. India. The Competition

Founders are NOT operating in a vacuum. Neither do VCs. A global fund is crunching the numbers as it will decide where to invest the money of 100m in Asia. One important, large number in the corporate tax-FDI row on the spreadsheet is the long-term impact of corporate tax on FDI.

Traditionally, capital flow going to Asia had had a small number of petting zoo Singapore (global hub), Vietnam (manufacturing gem) and Indonesia (the huge consumer market). India was seen as the high potential, and the high-risk cousin.

The factual comparison below highlights how the corporate tax rate stands against regional peers:

| Country | Headline Corporate Tax Rate | Key Incentives for Foreign Investors |

| India (Existing Co.) | ~22% (plus surcharge/cess) | No DDT. Stable regime. |

| India (New Mfg. Co.) | ~15% (plus surcharge/cess) | Globally one of the lowest rates. |

| Vietnam | ~20% | Multiple tax holidays and incentives, but a 20% baseline. |

| Indonesia | ~22% | Standard rate, with some incentives for specific sectors. |

| Singapore1 | ~17%2 | Low rate + extensive incentive schemes.3 |

The analysis opinion herein is as follows: It is not only about the headline rate.

- The 15% Game-Changer: When a startup has a component that is related to Make in India, as in the case of Make in India, whether it be a hardware business or EV, deep tech, drones, even advanced food processing, the 15% base corporate tax rate (for the new manufacturing companies formed after October 1, 2019) is unbeatable. Now, India would be more aggressive than Vietnam in terms of Corporate tax rate when it comes to manufacturing in India vs. Vietnam.

- The Stability Factor: The confidence of CFOs and policy analysts is due to the DDT’s elimination and the transition towards a more basic regime. The new gold is not being unpredictable, it’s being predictable.” Capital would like a 22% corporate tax rate which is not subject to fluctuation – a 17% which fluctuates with the turn of a political cycle is not desirable.

- The “China Plus One” Tail-wind: Tail-wind in Global supply chains. That’s a fact. There must be a welcome turf in Capital. The nice thing about this tax regime is the competitive corporate tax rate. It’s converting political tail wind to financial tail wind!

This shift, as recently mentioned by Economic Times is a huge part of the reason that India has been able to keep FDI inflows steady even during the recession, the world is currently in. The fact that India is no more the expensive outlier is evident. It is competitive and that’s where you go. The positive impact of corporate tax on FDI is definitely becoming evident.

Tax Provisions You Can not ignore about FDI as a Startup Founder.

So, now let’s get to the things that you can do. You are a founder, about to go for your Series A and negotiating with a fund from London. One needs to plan one’s business to benefit from the tax benefits at the time of startup in India.

Your CA is not only a compliance person, he/she is your strategic partner. The following are three things that you must have in your arsenal.

1. The 80 IAC Tax Holiday: Your Three Year Profit Shield.

This is the giant one among the startups recognised by DPIIT. It is a 100% deduction of profits on profits for the 3 years within the 10 year life cycle.

Analyst Insight: In my experience, 9 times out of 10, new founders at the initial stage get this wrong. They are so happy that they get it at the time of their paltry or zero profits, in Years 2, 3 and 4.

Don’t do this.

This is a decision that is made strategically. You spend your money, build your product and you have your market. When you’ve just attained some kind of good profit, which can be Year 6, 7 and 8, you pull this lever. You basically get three years of high profitability without having to pay any taxes on it and then you can use that money to increase the growth. This greatly accelerates the compounding effect in a VC’s eyes.

2. Carry Forward of Losses: The resilience Clause.

Startups burn cash. That’s the model. The same is also referred to as growth investments. The taxman has declared it a “loss”.

The good news? In most cases of startups (where continuity of shareholder is taken on board), you can carry forward these losses to the future profits to business.

When your losses are your losses as an accumulated asset, it is because a US Investor cares when creating a valuation model (such as a DCF). They are “tax shelters.

3. SEZ / GIFT City Benefit: The Construction of a Global Hub.

Is your company a global FinTech, B2B SaaS or DeepTech start-up? Don’t just set up in a non-personal co-working space. Work of Special Economic Zone (SEZ) or rather Gujarat International Finance Tec-City (GIFT City) has to be taken into consideration.

The benefits are staggering:

- Tax Holidays: The export profit holiday (with certain exceptions) for a number of years.

- GST Exemption: goods/services imported to SEZ/GIFT City unit will be exempted from GST.

- Financial Hub: GIFT City is in the process of being developed as a global financial hub, although the rules applied have been made more similar to Singapore or Dubai than to the Indian mainland.

Once we had a customer who was in the FinTech sector, who moved their back-office to GIFT City. They were able to cut down their effective tax rate on export earnings to single digits. It’s not an optimization that is a structural benefit. Tells your foreign investors that you are developing a “world first” business from day one.

Myth vs Reality: The Busting of Mainstream FDI Tax Fears

When I’ll converse with foreign funds, I find the same old fears. These are the Gluey stories that are obsolete.

Myth 1: The tax system of India is still a raid raj. Too extreme and controversial.

Reality: It’s a problem of the 2010’s. Is it perfect, look? No tax system is. The standardisation of India corporate tax rate and the introduction of the (relatively) stable GST regime, however, has taken away 80 per cent of the up and down. The focus, as evident in the NITI Aayog paper, has been definitely shifted from incentives that are policy oriented to action oriented. External Goal: Connect to the site of NITI Aayog/Applicable Strategy paper.

Myth 2: “My Singapore holding company takes care of all my tax related matters.”

Reality: The Singapore Flip. It was the default. But this is being subjected to a lot of criticism in the post-BEPS (Base Erosion and Profit Shifting) world. The tests of Substance over Form and GAAR (General Anti-Avoidance Rule) are applicable by the international tax authorities like India.

With your entire company, your IP and your market in India, having a shell company in Singapore is no longer the answer. In most instances, it is no longer less complex and risky. In many situations, it is now more affordable, cleaner and more secure to reside in India especially with the new Startup Funding India tax incentives.

Myth 3: “There is something that I have heard and heard about and that is Angel Tax. Won’t the loss of my funding be the end of me like that?”

Reality: The truth of the angel tax (under Section 56(2)(viib)) was indeed a big headache. This was a bad regulation which punished startups in valuation. However, the government has come to a big time savior. Starting from now, the recognized startup will be exempt provided that a simple declaration is done by the startup. The latter is a problem that has been addressed to a great extent in relation to a valid and sound start-up. Worrying about the past will doom 2026 fundraising efforts.

The 2026 Horizon: What comes next to Policy Analysts and Founders?

What will we be doing in 2026 then? India is using tax policy as a weapon of offense – a first-mover – to attract capital and not just for revenue collection. This is evident from the comparison of India vs. Vietnam Corporate tax rates.

For Founders: Tax compliance must be the next step in becoming tax strategy. Your tax structure is included in your product. Construct it in an efficient manner and you will have more partners. In such a way you can attract foreign investment in India 2026. The Net Profit After Tax is more than a snapshot of your MRR; it’s something that you can control and value on. Structuring your business properly is the most effective way to attract premium foreign investment in India.

For Policy Analysts: It’s another form of a game. The battle is not the same as it was in the past to cut rates. It’s “providing certainty.” The second jump will be in streamlining of the processes of administration, further streamlining GST and ensuring that the new Direct Taxes Code (when it comes) entraps this pro-growth position. As per a recent report by the RBI on capital flows the ‘Ease of Doing Business’ index, and ‘Ease of Paying Taxes’ are now directly associated as an implication. RBI Publication on FDI.Citation of an external resource from RBI about FDI.

Frequently Asked Questions (FAQs)

This will depend on your business. The effective rate for most of the non-existent domestic companies is about 25.17% (22% base + surcharge and cess) while for the new Domestic manufacturing companies (after 1st October, 2019) it is 17.16 (15% base + surcharge and cess). However, in case of startups which are recognised by DPIIT, it could be 0 on profits for 3 out the 80-IAC selected years.

No. The rate is hiked (approximately 40 percent) in case a foreign company is engaged in business in India (for example in the form of a branch office). This is why Indian foreign investment is invariably made through an Indian subsidiary (as a private limited company) that can enjoy the benefit of the lower rates in India.

While there isn’t anything specific that can lower it to 17% in Singapore, other incentives can bring it down significantly, whereas India has headline rate of 15% (effective 17.16) on new manufacturing and 80-IAC holiday which is more aggressive for new ventures eligible. The best place to be is no longer simply a response but it needs to be analysed.

Yes. This is certainly better for foreign investors, as opposed to the company paying DDT, the dividend has been taxable in the hands of the shareholder. This single shift significantly lowered the friction for international funds, making localized startup funding India tax incentives far more lucrative under global Double Taxation Avoidance Agreements (DTAA).

Conclusion: The Opportunity is Here. Are You Ready to Act?

We started off with founder’s nerves. And lastly the optimist of the analyst.

The India corporate tax rate change is not a one-off change in the rate of sales, but re-pricing the Indian market. The entire gamut of risk faced by India is being systematically dismantled and the first step is P&L. To win foreign investment in India, investors need to be aware of these changes.

The “Welcome Mat” is on the ground. It is no longer polluted, and the door is open by the government.

For those who’ve been around since 1985, and for those who can’t see the forest for the trees, it’s an opportunity… it’s a historic opportunity. It’s not a question of finding India to be a good bet anymore, it is whether your structure is good enough to go and capitalize on it.

Follow us On Linkedin, Instagram and Facebook for more content like this